Top Takeaways From the Annual Report on the SEC’s Whistleblower Program

On November 15, 2024, the Office of the Whistleblower at the U.S. Securities and Exchange Commission (SEC or the Commission) issued its annual report to Congress for the fiscal year (FY) 2024 (the FY24 Whistleblower Report). The data from the report indicates that the program has likely peaked in terms of whistleblower tips reported to the Office of the Whistleblower from around the world, but the SEC continues to pay out large awards at a steady pace. While the incoming Trump administration will change the focus of SEC enforcement, whistleblower tips will continue to have an impact on the cases brought by the SEC.

This Advisory includes our top takeaways from the report and insights from former senior leaders and staff from the SEC including Jane Norberg, who was Chief of the Office of the Whistleblower in the Division of Enforcement; Dan Hawke, who led the SEC’s Market Abuse Unit and was Director of the Philadelphia Regional Office; and Christian Schultz, who was Assistant Chief Litigation Counsel in the Division of Enforcement.

1. A New Record in Whistleblower Tips — Or, Is It?

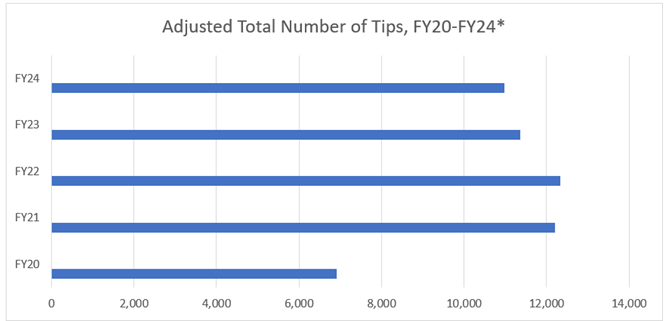

The SEC reported that it received approximately 24,980 whistleblower tips in fiscal year 2024, an increase from the 18,354 tips reported in FY23, which previously had been an all-time high for the program.1 The 2023 numbers had in turn been a dramatic increase from a total 12,322 tips in FY22, reflecting what appeared to be a trend of rapidly increasing use of the whistleblower program.2

But this year’s report came with an important asterisk.

The FY24 report noted that of the 24,980 tips submitted, over 14,000 were attributable to just two individuals.3 The report also noted an important data point not previously included in the FY23 report: of the 18,354 tips in 2023, nearly 7,000 also came from those same two individuals.4

These numbers complicate the story of the growth of the program over the last few years. For example, if one takes away the tips provided by the two individuals, the number of tips between 2022, 2023, and 2024 is far more consistent, and the numbers potentially represent slight yearly declines since 2022.

*The numbers for FY23 and FY24 necessarily reflect an approximation given that the SEC did not provide precise numbers for the tips submitted by two individuals.

This reflects the reality that, while tips increased immediately after much of the world shut down due to COVID-19, the tips actually leveled off in the years since. It also reveals a troubling pattern with anomalous but persistent tipsters who have figured out a way to spam the SEC’s Tips, Complaints, and Referrals system. Those anomalous tips distort the actual number of bona fide complaints and divert resources away from the SEC responding to actual fraud and harm to investors. Going forward, the SEC will need to figure out how to solve this problem.

Even so, the overall data of the last five years still represents a high number of tips and consistent use from whistleblowers, indicating that the program continues to be a reliable source of information for the SEC.

2. The SEC Aggressively Pursued Whistleblower “Impeding” Cases With Record Fines

In FY24 the SEC brought a record 11 actions under Securities Exchange Act Rule 21F-17, which prohibits taking steps “to impede an individual from communicating directly with the Commission staff about a possible securities law violation, including enforcing, or threatening to enforce, a confidentiality agreement.”5 The SEC brought more enforcement actions under this rule in FY24 than any other prior fiscal year, and this number was double the number of actions in FY23.6 The SEC had active “sweeps” in this area, bringing actions against a variety of public companies, investment advisers, and broker-dealers, including:

- Public Companies. In an enforcement “sweep,” the SEC announced settlements with seven public companies for using employment, separation, and other agreements that required employees to waive their right to possible whistleblower monetary awards.7

- Investment Advisors and Broker-Dealers. The SEC’s focus also extended to settlement agreements with investors. In a case that led to an $18 million civil penalty — the largest in a standalone 21F-17 case — the SEC found that an investment adviser’s settlement agreements with brokerage customers impeded whistleblowers by requiring clients to keep the underlying facts of the settlement confidential.8

In addition, the SEC settled charges with three affiliated registrants for actions taken to impede brokerage customers and advisory clients by asking them to sign confidentiality agreements that only permitted communications with the SEC if the SEC initiated the inquiry. According to the Commission, this violates the rule because it does not allow for voluntary outreach to the SEC by the customer.9

The SEC also settled an action against a registered investment adviser for language in non-disclosure agreements with employment candidates and settlement agreements with former employees requiring them to affirm that they had not reported possible violations to the law to any government agencies.10

3. Whistleblower Activity Leads to Large Awards — Some Reductions for Culpability

In FY24 the SEC awarded over $255 million to 47 individual whistleblowers. This represented the third highest annual amount of awards for the program.11 The size of these awards — one of which totaled $98 million and was split between two individuals12 — remains a strong incentive for individuals to report potential misconduct. However, not all of these awards were as large as they could have been as the SEC reduced three awards in FY24 due to the whistleblower’s participation in or benefit from the underlying misconduct. While the SEC does not say how the individuals were culpable, it is a reminder that even individuals who had a small role in the underlying action can receive an award. A whistleblower award also may be decreased if the whistleblower unreasonably delayed in reporting, or interfered with internal reporting systems.13

As noted in a recent Arnold & Porter Advisory anticipating changes to the Commission’s approach to federal securities law enforcement under the Trump administration, the SEC may shift its approach to making awards in the future. Current Republican commissioners have voiced objections to award amounts and a lack of transparency regarding the award process. While awards paid to whistleblowers must fall within a statutory range of between 10% and 30% of the amounts collected,14 the Commission could increase scrutiny of how percentages are calculated or use its rulemaking authority to take the dollar amount of the award into account in determining the percentage of a whistleblower award.

4. Manipulation, Offering Fraud, Disclosures and Financials, and Cryptocurrency Remain Top Allegation Categories

The most common whistleblower tips received by the SEC in FY24 include allegations of Manipulation (37%), Offering Fraud (21%), Corporate Disclosures and Financials (8%), and Cryptocurrency (8%).15 We note, however, that these percentages are skewed in favor of whatever category (likely manipulation) that the anomalous tipsters selected when they submitted their 14,000 tips. Unfortunately, the SEC did not back the 14,000 anomalous tips out of the allegation categories to give a truer picture of legitimate tip categories.

This year’s total of 1,994 crypto and ICO-related tips reflects crypto’s continuing permanence as a focus for whistleblower complaints. But the regulatory environment around cryptocurrencies and assets may be changing. As noted in the Arnold & Porter Advisory discussing the new Trump administration’s anticipated enforcement priorities, we expect to see a return to bread-and-butter enforcement and, except for outright fraudulent conduct (to the extent such conduct can be tied to actual securities), less focus on cryptocurrency and digital assets.

5. The Whistleblower Program’s Reach Remains Global and Company Outsiders Get Rewards

As with prior years, the FY24 report shows that the whistleblower program continues to have a global reach, with tips coming in from all around the world. Outside of the United States, the highest number of tips came from Canada, the United Kingdom, India, Australia, and Germany.16 In addition to the global reach, whistleblowing under the SEC program is not limited to company insiders, such as employees or former employees. Whistleblowers can be individuals outside the organization, such as investors or potential investors, competitors, or market observers. The FY24 report indicates that while 62% of whistleblowers receiving awards this year were insiders, 38% were outsiders.17

Recommendations for Companies

The FY24 report reflects the continued importance of whistleblowers to the SEC’s overall enforcement program, and the large monetary incentives under both the SEC’s program and that of the new whistleblower program from the U.S. Department of Justice highlights the need for companies to take action promptly once they receive an internal report of potential misconduct. Entities should consider the following risk management steps.

Internal Reporting Framework

Review your internal reporting procedures, controls, and framework. Make sure that all reports — including those reported to a direct supervisor and not just those going to an internal hotline — are captured, triaged, and investigated, if appropriate. Companies that are able to conduct thorough internal investigations showing a clear, robust response to an internal tip will be better able to effectively self-correct and have a defensible position if regulators or law enforcement become involved.

Internal Investigations

Early acknowledgement and appropriate follow-up communications with an internal reporter are important. Lack of communication after a tip is submitted can result in misunderstandings or whistleblowers believing that internal reporting is futile.

A company will want to fully understand the issues raised by the internal reporter. This should be one of the first interviews conducted by the company. Try to preserve the confidentiality of the reporter as much as possible during the internal investigation to ensure integrity and trust in the internal reporting system.

Consider how to preserve attorney-client privilege over ensuing investigations and when to brief senior management, the audit committee, and the full board of directors about an internal whistleblower.

Review Documents for Language That May Impede Government Reporting

Given the SEC’s continued aggressive enforcement of Rule 21F-17 actions, thorough and expansive reviews should be conducted to ensure the company is not using documents that the SEC could interpret as limiting or impeding an individual’s right to communicate with the Commission. Documents that should be reviewed include (but are not limited to) investor documents, severance agreements, confidentiality agreements, settlement agreements, compliance manuals, intellectual property agreements, and training materials. Importantly, be sure to review any documents that contain confidentiality provisions.

Anti-Retaliation Policies and Training

Ensure that whistleblower anti-retaliation policies and training are up to date. Misunderstandings can lead to costly lawsuits against a company. Annual training should be conducted to ensure that everyone understands that retaliation can fall well short of outright firing.

Domestic and International Policies

Companies should update both domestic and international policies. As the whistleblower program continues to have a global reach, companies that operate overseas should take into account the possibility of foreign SEC whistleblowers when considering internal compliance policies, procedures, and training, and take into account any local cultural norms and laws that might discourage internal reporting.

Conclusion

The FY24 report demonstrates that the whistleblower program remains a priority for the SEC, and will likely remain to be so during the Trump administration. Whistleblower tips continue to drive SEC enforcement actions and impose high costs on companies. Companies will need to remain proactive and have appropriate mechanisms in place to identify and promptly investigate and correct any potential misconduct before it is reported to the SEC.

© Arnold & Porter Kaye Scholer LLP 2024 All Rights Reserved. This Advisory is intended to be a general summary of the law and does not constitute legal advice. You should consult with counsel to determine applicable legal requirements in a specific fact situation.

-

FY24 Whistleblower Report at 11 & n.32; see FY23 Whistleblower Report at 1, 5.

-

FY23 Whistleblower Report at 5.

-

FY24 Whistleblower Report at 11.

-

-

FY24 Whistleblower Report at 1; 17 C.F.R. §§ 240.21F-17(a).

-

FY24 Whistleblower Report at 1.

-

-

-

-

-

-

-

-

See 15 U.S.C. § 78u-6(b)(1)(A)-(B).

-

FY24 Whistleblower Report at 11-12.

-

-

Key Contacts